Why Fortune 500s and safety-focused businesses use captive insurance for smarter, more predictable coverage.

As a business owner, you’ve likely faced the same frustrating cycle year after year. Your insurance renewal arrives, premiums have increased again, and you’re left with little choice but to pay. You’ve spent countless hours on safety training, risk management, and prevention efforts, yet the benefits rarely impact your bottom line. Instead, your efforts seem to boost the insurance company’s profits.

What if, instead of sending premiums out the door without anything to show for it, those same dollars could build something lasting and profitable for you? This illustrates the power of Captive Insurance. Unlike traditional insurance, where you’re vulnerable to market fluctuations and carrier decisions, a captive allows you to design an insurance program to fit your business, risks, and financial objectives.

Think of the difference between renting and owning a home. Renting means less control and no equity, while owning requires a bigger upfront commitment but allows you to build long-term value. Traditional insurance is like renting; premiums are paid and never come back. A captive is like homeownership; your investment works for you, providing stability, control, and the chance to capture profits that would otherwise go to someone else.

In this article, we’ll break down what captive insurance really is, clear up common misconceptions, explain why some businesses are a perfect fit, share real-world examples, and highlight why it’s worth owning instead of renting when it comes to insurance.

Navigation Guide

- What Is Captive Insurance?

- Why Are Some People Afraid of Captive Insurance?

- Who Makes a Good Candidate for a Captive?

- Why Should Businesses Be Interested?

- Group Captives vs. Single-Parent Captives

- Real-World Examples

- The Real Goal of a Captive

- How to Get Started

What Is Captive Insurance?

Captive insurance is when a business sets up its own insurance company to cover its risks. Instead of purchasing a policy from a traditional insurer, it creates a company that insures itself. This means you’re not paying premiums into a void; you’re building something you control. If claims are low, you keep the profits. If claims are high, you still have more visibility and control over how they’re managed.

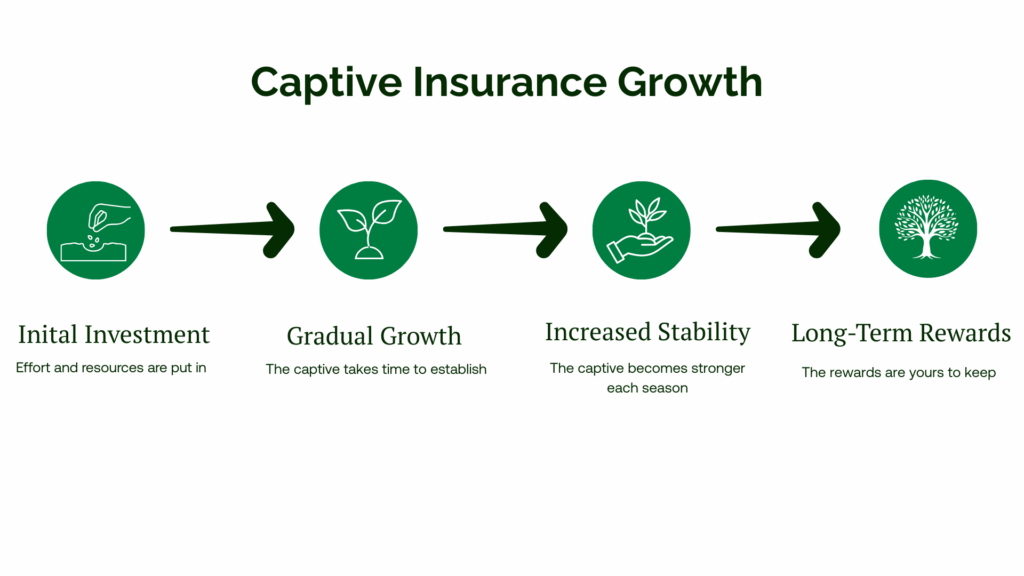

Think of it like planting an orchard. It takes effort and investment at first, but once the tree grows, you can harvest it year after year. The tree won’t produce fruit immediately, but gradually, the orchard becomes stronger each season, providing more stability and yield. A captive works the same way. It takes time to establish, but the long-term rewards are yours to keep.

Why Are Some People Afraid of Captive Insurance?

It’s no secret that captives have a reputation problem, mainly because of how microcaptives were misused under IRS section 831(b). These small captives were sometimes set up as tax shelters rather than legitimate risk management tools. The IRS cracked down and penalized those who took advantage, creating fear and confusion.

But here’s the key difference: A well-managed captive, built for true risk management, is not only compliant but a solid foundation for your insurance strategy.

Captives fail when companies:

- Cut corners to save upfront costs.

- Focus only on tax advantages instead of true risk transfer.

- Enter without strong loss control or with too many claims already on their record.

Do it right, or don’t do it at all. That’s the golden rule. When properly structured, captives have been used successfully by most Fortune 500 companies and mid-sized businesses in industries like construction, trucking, manufacturing, and hospitality for decades.

Who Makes a Good Candidate for a Captive?

Not everyone can, or should, own a captive. It’s like buying a house. You need the financial readiness to handle the upfront investment and ongoing responsibilities.

Good candidates typically have:

- Premiums over $500,000 per year: This amount varies depending on the captive’s size, structure, and the types of risks covered. It can range between $250,000 and $1 million on average.

- Financial stability: The ability to make a capital investment. The initial costs for the first year are higher, but you will save more money in the long run. Think of it as a down payment on a house. You pay 20% upfront, but avoid the PMI.

- Outstanding safety control: If your company already prioritizes safety, training, and risk prevention, you’re ahead of the game. Captives reward companies that actively manage risk and losses.

- Low claim frequency: Frequent claims are a red flag. A history of low loss ratios signals a captive might be a good fit.

Industries like wholesale, construction, trucking, and manufacturing are a natural fit because businesses often pay millions in premiums but also prioritize safety. POWERS® Insurance & Risk Management helps companies assess readiness upfront, so they don’t waste time pursuing a strategy that won’t fit.

Why Should Businesses Be Interested?

Captive insurance offers benefits that traditional insurance cannot:

- You keep the underwriting profits. In traditional insurance, carriers build additional costs such as marketing, commissions, and general overhead. In a captive, the profit margin belongs to you.

- Stability in a hard market. Insurance costs are recurring; sometimes premiums spike for reasons outside your control. Captives help “smooth out” the ups and downs. Instead of riding the wave of market fluctuations, you get steady, predictable costs.

- Better control of claims. A captive keeps you closer to the claims process. You understand where the money is going, how losses are being managed, and you’re motivated to reduce risks.

- True ownership of your insurance program. You’re building equity in your own insurance structure.

- Additional Investment Income. Captives invest claim reserves, which can produce consistent returns. Over five years, if the program is managed properly, it’s common for a captive to return six figures to its owners.

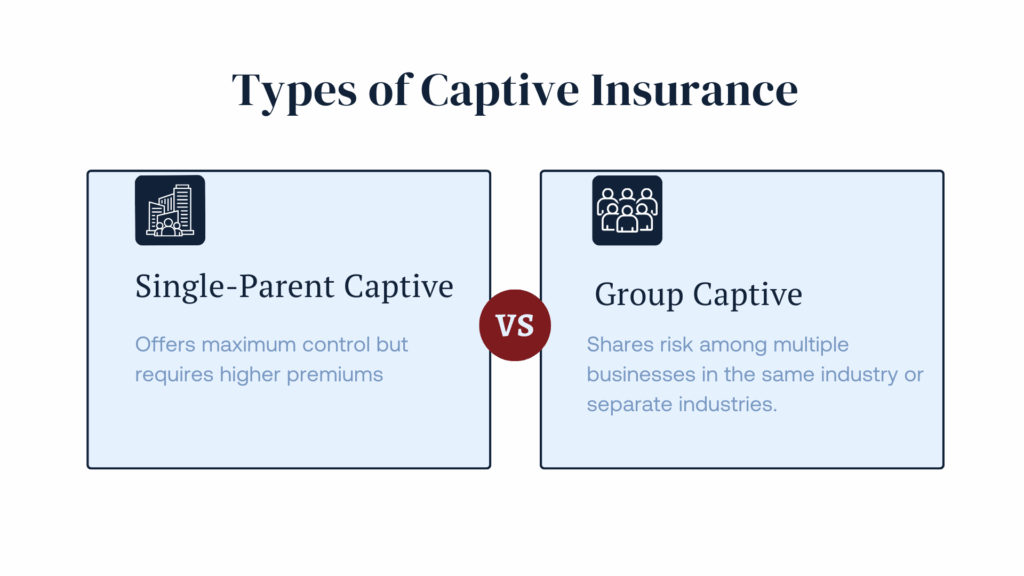

Group Captives vs. Single-Parent Captives

There are two main captive structures businesses typically consider:

- Single-Parent Captive: This is your own insurance company, created exclusively for your business or a group of related businesses. It offers maximum control but requires higher premiums and a stronger financial standing.

- Group Captive: This involves multiple businesses coming together to share risk. There are two types:

- Homogeneous group captives (companies from the same industry, such as construction firms)

- Heterogeneous group captives (companies from different industries, like a trucking company and a manufacturer)

With a group program, everyone’s loss history contributes to the overall pricing. This encourages participants to improve loss control, as poor performance can increase costs for all.

POWERS® Insurance guides clients through these options by conducting detailed feasibility studies. This helps you determine whether owning outright or partnering with others makes more sense.

Real-World Examples

Construction Companies

Take a large construction company that pays millions in premiums annually. Traditional insurance often spikes after a few tough years in the industry, even if the company maintains strong safety practices. They are essentially penalized for being part of a high-risk industry.

By creating a captive insurance company, that same construction firm shifts the narrative and takes control. Since it’s invested in safety programs, training, and strict job site protocols, its claims tend to be lower than the industry average. In a traditional insurance setup, it wouldn’t see much benefit. But with a captive, those reduced claims lead to lower costs and potential profit opportunities.

It’s like paving your own road instead of relying on a pothole-filled highway. You invest upfront, but the smoother ride pays off over time.

Manufacturing Companies

Manufacturers often face high workers’ compensation costs, product liability, and property coverage for large facilities. A mid-sized manufacturer paying over $500,000 in annual premiums might see rates increase due to broader industry issues, even if its own safety record is excellent.

By joining a group captive, the manufacturer pools risk with other like-minded businesses. Since it has invested heavily in machine safety, employee training, and preventative maintenance, its claims stay low. In the captive, that discipline pays off. Instead of subsidizing the poor performance of others, it shares in underwriting profits.

Hospitality Businesses

Restaurants, hotels, and casinos face risks ranging from guest injuries to liquor liability. These businesses often struggle with unpredictable premiums, especially in states where litigation is common.

A regional hotel group might decide to form a captive after years of steep premium increases. The group would eventually reduce claims by implementing strict safety standards, such as slip-resistant flooring, staff alcohol training, and robust security measures.

The Real Goal of a Captive

Captives aren’t a quick way to save money. They focus on stability, ownership, and long-term financial health. We’re currently in a hard insurance market. Rates across nearly every line of coverage are increasing rapidly, and markets are becoming more selective. Many businesses feel like they’re paying more for less protection.

If that’s how you feel, joining a captive can eliminate the unpredictable costs of premiums and provide you with stability.

How to Get Started

Captive insurance isn’t for every business. It requires commitment, financial strength, and a culture of safety. However, for the right companies, it can be a game-changer. At POWERS® Insurance, we often say, “Captives don’t save you money in year one. They build value over the next ten.”

If rising premiums are squeezing your business, it may be time to explore a captive.

POWERS® Insurance can assist your company in shifting from being “insurance renters” to “insurance owners” with the right structure. Our process is simple:

- We Listen First

- We Run the Numbers

- We Help Build the Right Path

- We Stay Involved

Reach out to POWERS® Insurance today to find out if captive insurance is a good fit for your safety-focused business.